ADU Insurance in San Jose, Sunnyvale & the Bay Area: What Homeowners Get Wrong About Coverage

Your homeowner's policy probably doesn't cover your ADU the way you think it does. Here's what I've learned about the insurance gap after managing 150+ ADU tenancies across San Jose, Mountain View, Sunnyvale, and Palo Alto in Santa Clara County.

I've managed over 150 ADU tenancies across the South Bay. In that time, exactly two have resulted in insurance claims. Both times, the homeowner assumed their existing policy covered the ADU. Both times, it didn't. One of them ended up paying $14,000 out of pocket for water damage that a $200-a-year rider would have covered.

It keeps happening. Owners in San Jose, Mountain View, Sunnyvale, Palo Alto. They spend $350,000 building a detached ADU, run the numbers on what it'll earn, find a tenant, and never once check whether their insurance actually covers the thing.

Your homeowner's policy probably has a gap

A standard homeowner's insurance policy covers your primary residence and provides some liability protection if someone gets hurt on your property. But that liability coverage typically applies to guests, not tenants. And the structure coverage often doesn't extend to a separate building unless you've explicitly added it.

It depends on what you built:

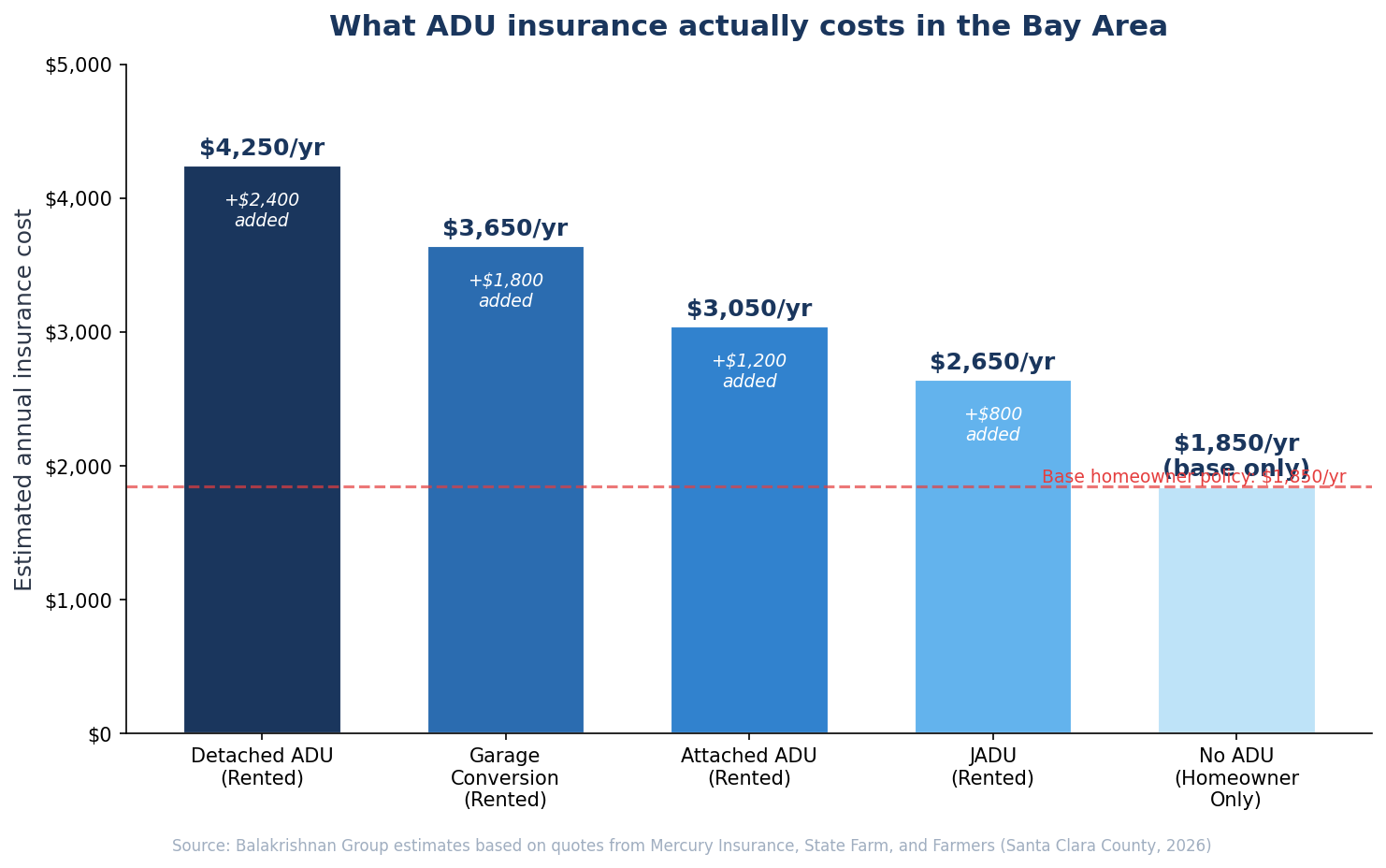

Detached ADUs are the biggest gap. They're a separate structure on your lot. Most homeowner's policies either exclude them entirely or cap "other structures" coverage at 10% of your dwelling coverage. If your house is insured for $1.5 million, that gives you $150,000 for your ADU. A well-finished detached ADU in Santa Clara County costs $350,000 to $550,000 to build. Whether you're in San Jose's Willow Glen neighborhood, a Campbell lot near Pruneyard, or a Cupertino cul-de-sac near Apple Park, the math is the same: you're underinsured by default.

Garage conversions fall into a gray area. The structure was already part of your policy when it was a garage. But converting it to a living space changes its risk profile. If your insurer doesn't know about the conversion, a claim could be denied.

Attached ADUs are more likely to fall under your existing policy since they share walls and infrastructure with the main house. But "more likely" isn't "guaranteed." If you added square footage, changed the use, or installed a separate entrance, your policy may need updating.

JADUs (Junior ADUs built inside the existing house) are the simplest case. They're within the footprint of your home and most policies will cover the structure. But you still need landlord liability coverage once a tenant moves in.

The liability problem is bigger than the structure problem

Let's say a tenant slips on wet stairs outside your detached ADU and breaks their wrist. Or the water heater fails and floods the unit, destroying the tenant's laptop and furniture. Or there's an electrical fire in a panel that was installed during the ADU build.

If you're renting the unit and you don't have landlord liability coverage, your homeowner's policy will likely deny the claim. Standard homeowner's liability is for social guests, not paying tenants. The legal distinction matters when a claims adjuster is looking for reasons to say no.

A landlord protector policy, sometimes called a dwelling fire policy or a landlord insurance policy, fills this gap. Most come with $1 million in liability coverage and cover the standard stuff: fire, smoke, vandalism, water damage, and the landlord's legal liability for tenant injuries. They run $800 to $2,400 a year in the Bay Area depending on the ADU type and coverage limits. I wrote about the full economics of ADU rental income separately, but the short version is that $200 a month in insurance is a rounding error against $3,000 a month in rent.

What to do if your ADU is unpermitted

This gets harder. If your ADU was built without permits, most insurers won't cover it as a rental unit. Some won't cover it at all. The risk profile for an unpermitted structure, where the insurer can't verify that electrical, plumbing, and structural work meets code, is too high.

I wrote a detailed guide on legalizing unpermitted ADUs that covers the AB 2533 pathway, costs, and timeline. If you're renting an unpermitted unit without insurance, you're carrying all the risk yourself. A tenant injury, a fire, a flood, and you're on the hook for all of it.

Getting the unit permitted also opens up your insurance options. Once you have a certificate of occupancy, you can get proper landlord coverage, and the cost is actually reasonable.

What I tell every ADU owner in San Jose, Mountain View, and Palo Alto

Before your first tenant moves in, do three things:

Call your insurer. Tell them you've built an ADU and you're renting it out. Ask specifically whether the structure is covered and whether your liability extends to a paying tenant. Get the answer in writing.

Get a quote for landlord coverage. If your existing policy doesn't cover the rental scenario (it probably doesn't), get a quote for a standalone landlord policy or a rider. Mercury, State Farm, and Farmers all write these in Santa Clara County. We've also seen competitive quotes from AAA and USAA for properties in Sunnyvale, Mountain View, and Campbell. Shop at least three.

Match your coverage to the build cost. If you spent $400,000 building a detached ADU, don't accept $150,000 in "other structures" coverage. Make sure the policy covers the replacement cost of the unit, not just some default percentage of your dwelling coverage.

If you're managing the tenant relationship yourself, I covered the dynamics of living next to your tenant in a separate post. Insurance is one piece of that puzzle. The lease, the shared-property addendum, and the screening process all work together to protect you.

Whether you own a garage conversion ADU in San Jose, a detached backyard unit in Mountain View, or a JADU in Campbell, the insurance playbook is the same: call your carrier, get the rider, and match coverage to replacement cost.

And if you're still weighing whether the ADU makes financial sense at all, the complete guide to renting out your ADU covers everything from permits to pricing to management.

If you have an ADU and want a straightforward assessment of your rental setup, including insurance, pricing, and management, request a free ADU rental analysis. I'll tell you what I see based on 12 years of doing this in the South Bay.

Sources

- ADU Insurance in California: What Homeowners Need to Know — Better Place Design Build

- Garage Conversion and ADU Insurance Info for 2026 — GreatBuildz

- ADU Insurance in California: Understanding Options — SnapADU

- Accessory Dwelling Units: Understanding ADUs — Mercury Insurance

- ADU Insurance: What All You Need to Know — Bay Area Property Management

- California's 2026 Housing Laws: What You Need to Know — Holland & Knight

Ready to manage your ADU?

Get a free rental analysis. Three-day turnaround. No obligation.

Request a Free Analysis →